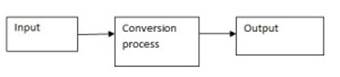

It is a step by step value addition process of converting one form of the material into another form, to increase the utility of the product for the user.

Production system:

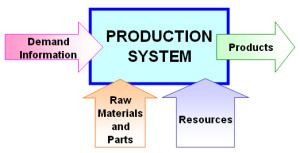

It is an organized process of converting the raw material into final product with the help of the feedback loop.

Productivity:

It is a quantitative ratio, between what we produce and what we use as resources to produce them. Every organization always wants to increase the productivity by applying new techniques and methods.

Industrial engineering:

Industrial Engineering is concerned with design installation and improvement of production system. The objective is to eliminate unproductive operations from the production system in order to increases the productivity.

Production manager

Production manager is concern with planning, controlling and directing the day to day life working of production system. The objective is to produce goods and services of right quality plus at a predetermined time and cost.

Cost in production:

The cost in production is divided into two types they are

- Direct cost or Prime cost

- Factory expanses or factory overhead

- Factory cost

- Total cost

- Sale cost or selling cost

Direct cost:

Direct cost includes the direct material, direct labor and direct expenses.

Factory Overload:

- Factory overload is also known as factory expanses. It consists of indirect material, indirect labor and indirect expenses

- In the indirect material it consists of cutting fluid, lubricant and stationary items

Indirect labor

- Indirect labor consists of supervisor, higher officials etc.

- Indirect expenses consists of electrical bills, telephone bills, facility provided

- Factory cost includes the primary cost and factory overhead

Total cost

Total cost consists of factory cost, marketing, advertisement and transportation etc.

Selling cost

Selling cost is also known as sale cost. It includes total cost and profit.

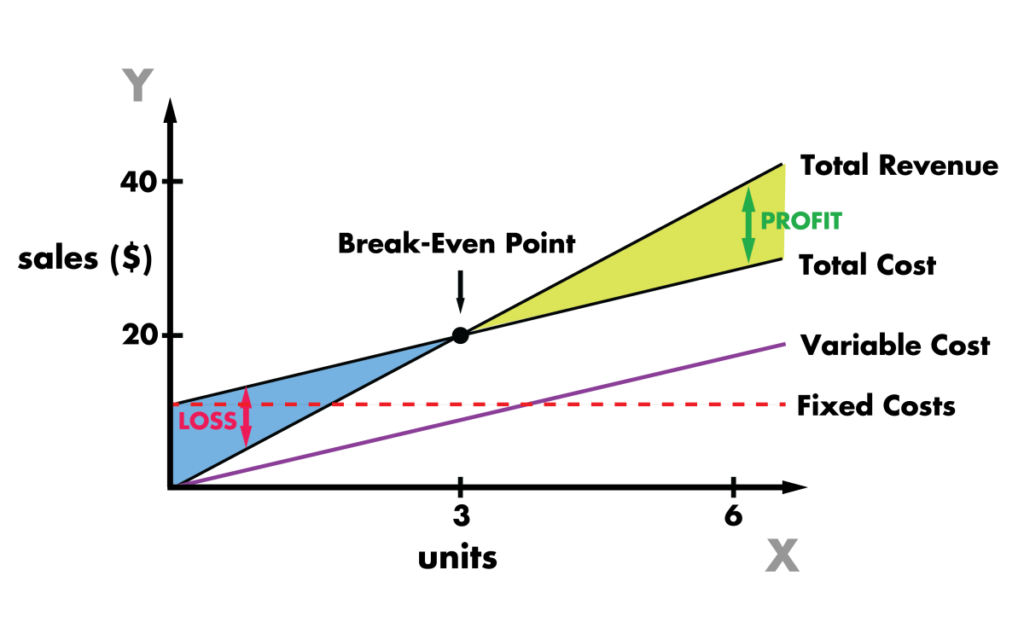

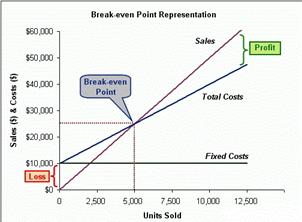

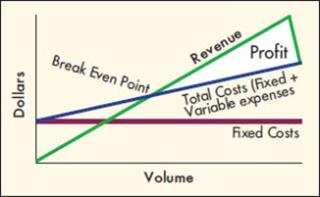

Break even Analysis:

The break even analysis consists of three parts. They are

- Total cost

- Selling cost

- Volume of production

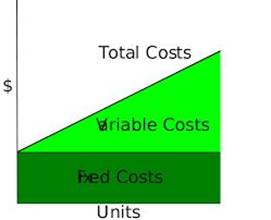

Total cost:

It indicates the total expenditure made in order to produce certain number of units and it is the sum of fixed and variable cost.

Fixed cost:

The cost remains constant or fixed irrespective of volume of production. It includes cost of machine, salary, higher officers, rent of building, advertisement cost, insurance cost, set up cost and interest etc.

Variable cost:

F= fixed cost

x= no. of units produced in order to earn profit of p

= variable cost per unit

= variable cost per unit

s= selling price per unit

S = total sales or revenue

Total sales:

A total sale is also known as total revenue. It indicates the return obtained by selling out the quantity to be produced.

Break even analysis chart:

Break even analysis point is the volume of production where total cost becomes equal to total sales, and organization neither earn profit nor suffer from loss. It is also known as no profit and no loss point.

Total sales= total cost + profit

s= F+V+P

Terms used in break-even analysis

Angle of incidence:

It is the angle at which total sales line cut the total cost line, higher this angle better the working conditions will be obtained.

Contribution Margin:

The contribution marine is the difference between the total scale and the total variable cost. The contribution margin is also called as margin profit or gross margin

Profit volume ratio:

It is the term used to represent the profitability related to scales. For a particular product this ratio remains constant, and is normally preferred when a company manufactures many products. It is the ratio of contribution margin to the volume of sales.

Margin of safety:-

Margin of safety is defined as the difference of output at full capacity compared to output at break-even point.

{kind=link}